'%3e%3cellipse%20cx='185.202'%20cy='292.401'%20rx='236.2'%20ry='212.4'%20transform='rotate(180%20185.202%20292.401)'%20fill='url(%23paint0_radial_6113_7068)'/%3e%3c/g%3e%3cdefs%3e%3cfilter%20id='filter0_f_6113_7068'%20x='-130.996'%20y='0.000976562'%20width='632.398'%20height='584.8'%20filterUnits='userSpaceOnUse'%20color-interpolation-filters='sRGB'%3e%3cfeFlood%20flood-opacity='0'%20result='BackgroundImageFix'/%3e%3cfeBlend%20mode='normal'%20in='SourceGraphic'%20in2='BackgroundImageFix'%20result='shape'/%3e%3cfeGaussianBlur%20stdDeviation='40'%20result='effect1_foregroundBlur_6113_7068'/%3e%3c/filter%3e%3cradialGradient%20id='paint0_radial_6113_7068'%20cx='0'%20cy='0'%20r='1'%20gradientUnits='userSpaceOnUse'%20gradientTransform='translate(-43.0144%20248.324)%20rotate(-25.0248)%20scale(462.733%20514.489)'%3e%3cstop%20stop-color='%23FF9DDA'/%3e%3cstop%20offset='0.44'%20stop-color='%23F7FF9D'%20stop-opacity='0.52'/%3e%3cstop%20offset='0.84'%20stop-color='%23FF8B7B'%20stop-opacity='0.2'/%3e%3cstop%20offset='1'%20stop-color='%23F7FF9D'%20stop-opacity='0'/%3e%3c/radialGradient%3e%3c/defs%3e%3c/svg%3e)

Most acquiring companies do a poor job of integration, which becomes clear when comparing median acquirers with high performers. One study found that “frequent acquirers,” or those with more repeated experience, were 130% more successful. In large part, this is because acquisitions and integrations unfold in unexpected ways. Opportunities reveal themselves, or plans go sideways and create new opportunities.

It takes an experienced operator to stay steady and know what to try next. And strong, unified financial data so the team is testing hypotheses and not just operating on instinct.

In this guide, we share examples of integration and the critical role that your ERP system plays in unlocking those cost, revenue, and financial benefits of parent-child entities.

The integration roadmap is almost never right

Skilled integrators are keenly aware of two things: They can’t know everything, so they must stay alert to possibilities. And two, successful synergy strategies are explainable in a single sentence. If you can’t say it briefly in plain speak, you don’t yet understand it.

Do you understand your present integration and all its potentials? You can test your understanding with a whiteboard. Diagram the process by which the two companies can support each other—the workflows, entities, and interactions. Anywhere that you find difficult to diagram—anywhere with question marks or blank spaces—those are areas to investigate through interviews and site visits.

Most of that learning happens firsthand, after the purchase, because the spreadsheet is never a sufficient view. “The map is not the territory,” said mathematician Alfred Korzybski, meaning, go walk the site. Alberto Griera, CFO of the global elevator manufacturer KONE, has a playbook for this: Identify the new company’s critical data flows and follow them back to the computers and people that input them. Ask those people what they do, what they use the numbers for, and who they interface with.

“If you want that information to lead to transformation—to use it to help various functional leaders be more effective—you need everyone to realize that their systems aren’t the ultimate truth,” he says. “And help them see that they are all part of a larger collection of systems.”

In doing this, you often come to understand that acquisition target in a new way. Due diligence is thorough, but it’s never like the firsthand understanding that comes with time. For example, when The New York Times acquired the tech review site Wirecutter, they intended to open up a new channel for affiliate revenue. But they gained an infusion of tech talent that then helped them build out an ecosystem of apps. It’s hard to know which is more valuable, but again, the benefits unfold.

One thing that makes this process particularly tricky is that acquisition targets often don’t know their own processes. It’s not that they’re hiding anything. People just haven’t gone through the metacognitive exercise of asking why they do what they do, and documenting how. This is extra work that most line of business leaders don’t have enough time for.

An example: When Dharmesh Shah, then running procurement at Uber, was tasked with evaluating the inventory systems for the newly acquired JUMP Bikes, he was startled to learn that all the tracking happened in Google Sheets. There were no controls. JUMP Bikes was losing millions of dollars of equipment every year.

As you complete enough integrations as an organization, you enter super-acquirer territory, where you spot more overlaps and benefits than another company would. You earn a higher success rate and greater individual successes. One of the best examples of this is the pharmaceutical manufacturer Danaher. The company evolved from a real estate trust into an acquirer of medical devices, which led them to a thesis and a proprietary work method that allowed them to complete 240 acquisitions over 25 years and grow the stock 10,000%.

This is all to say, don’t confuse the map with the territory. Don’t settle for your initial conception. Go walk the floors and enact the plan and know that the real plan will only ever emerge with time and attention.

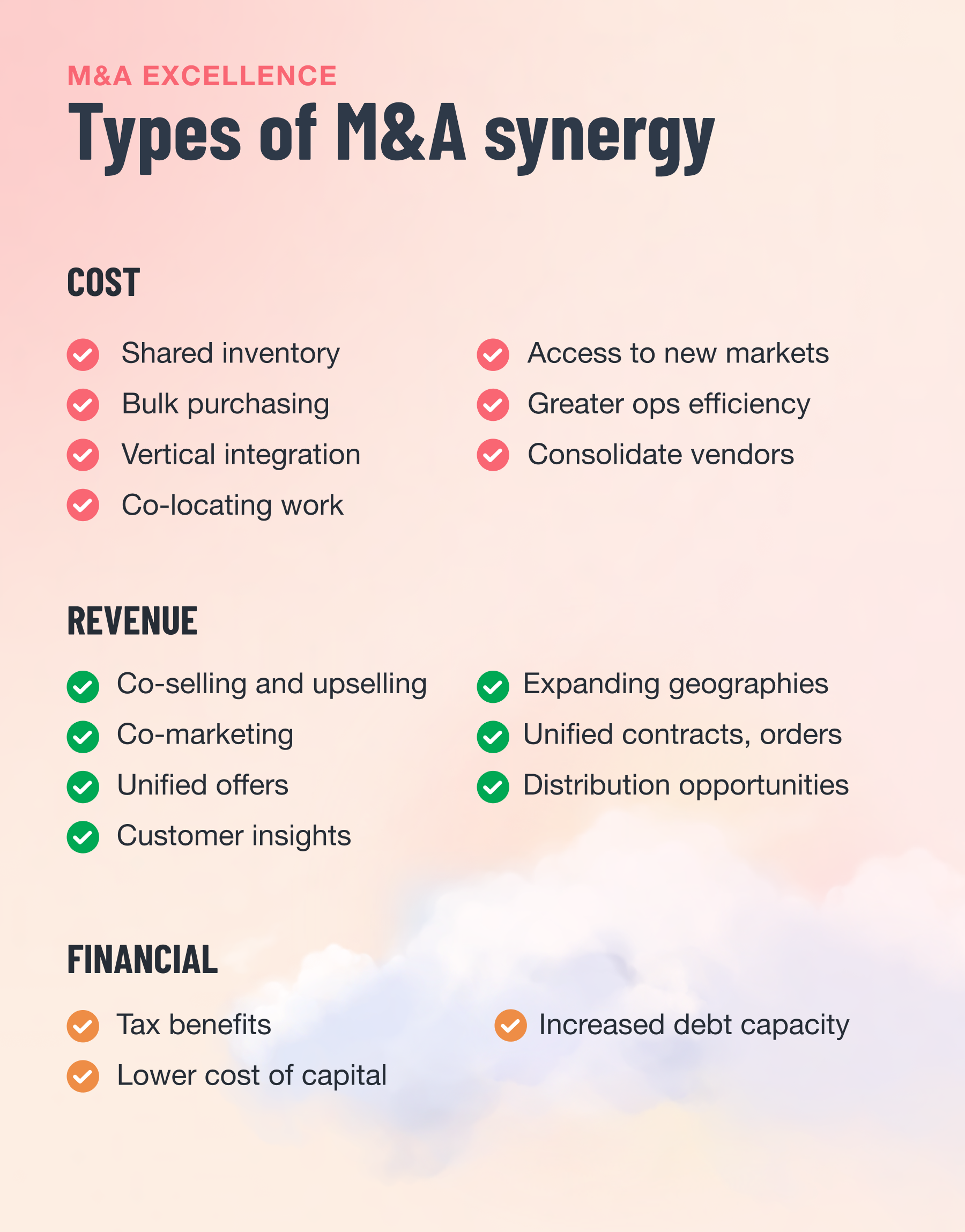

Great examples of synergy capture

MBA programs will teach you that there are three categories of synergy, but experience tells us that it’s rarely so clear-cut. Like the aforementioned example of The New York Times acquisition, you purchase a company for a set of reasons and find that list is much longer. The Times initially just enjoyed the affiliate revenue, but then realized it could pull the affiliate review articles into the overall paper without spooking readers, and then pull its CPM advertising model back over to the affiliate site.

A food distributor was able to launch unified promotions

In this example, the parent company integrated the specialty meat subsidiary so it could join in on one shared holiday promotion with the produce subsidiaries. And a unified services agreement made buying from all easier, earning the parent company more wallet share.

A media company diversified its revenue streams

An online magazine known for journalistic reporting bought an affiliate marketing site recognized for high-integrity reviews. The parent company pulled the reviews into its news app and its news articles into the review site. Eventually, they stretched the advertising network to cover both— mixing two advertiser audiences and increasing ad sales.

An elevator manufacturer integrates horizontally

This manufacturer acquired its top implementation partner. The goal was to shore up its own ailing professional services department, and also launch new products—which it did by co-building an app-based training software and predictive maintenance subscription. It then sold both into its global install base.

A national distributor unifies its pricing schedules

The national team wanted better insight into kickbacks and earned income on paper contracts. By using optical character recognition and phones and tablets to digitize all paperwork, they gained far more visibility into pricing schemas. They found significant savings by standardizing offers.

A big-box store upgrades its inventory tech

This chain acquired a small, tech-forward competitor and rolled its order inventory software out across all locations. This united online and in-store stock inventory data. For the first time, employees could confidently check inventory at other locations. This change recovered a few percentage points in leaked revenue.

A telecom company closes its commission loopholes

This company initially deferred integrating half a dozen acquired companies. But years in, they decided to complete the work as part of a modernization effort where they demolished the longstanding team silos: wired, wireless, and app. They united all sales teams into one and consolidated 12 legacy systems.

This produced immediate savings by eliminating longstanding loopholes where salespeople could pad their commission by canceling products in one system to reopen them as a new sale in another.

A jewelry store expands

This jewelry store chain perfected homegrown sales software and method for operating at theme parks. This technology and strong sales culture were a competitive advantage, and when they began acquiring smaller chains in different locations, they rolled out those systems and methodologies for an immediate sales lift at every location.

A healthcare system consolidates roll-up financials

This health system was on a spree of acquiring clinics and halted when the back office and accounting grew too complex; every clinic had its own P&L. Some clinics also owned other clinics. The period-end closes for the parent company started taking months. Leadership initiated a “year of efficiency” and moved all clinics onto one ERP that could handle many sub-entities and sub-ledgers.

The road to being a super-acquirer

It's estimated over thirty percent (or 11,000) of enterprises acquired last year will fail. But how much of that is avoidable? If you look at the habits of super-acquirers, it suggests a great many can actually beat those odds. Some of the biggest failures are the results of companies delaying or failing to merge or consolidate ERPs, and never gaining the multi-entity view of income and expenses. They never get to the point of unified primary services agreements to allow easy bundling, or real-time sales data to inform multi-entity promotions and offers.

That’s something you can partly address through instinct and experience. But a significant portion is entirely dependent on the flexibility and interoperability of your finance technology. Is yours built for change? That's where you'll find the most synergies—and success.