'%3e%3cellipse%20cx='185.202'%20cy='292.401'%20rx='236.2'%20ry='212.4'%20transform='rotate(180%20185.202%20292.401)'%20fill='url(%23paint0_radial_6113_7068)'/%3e%3c/g%3e%3cdefs%3e%3cfilter%20id='filter0_f_6113_7068'%20x='-130.996'%20y='0.000976562'%20width='632.398'%20height='584.8'%20filterUnits='userSpaceOnUse'%20color-interpolation-filters='sRGB'%3e%3cfeFlood%20flood-opacity='0'%20result='BackgroundImageFix'/%3e%3cfeBlend%20mode='normal'%20in='SourceGraphic'%20in2='BackgroundImageFix'%20result='shape'/%3e%3cfeGaussianBlur%20stdDeviation='40'%20result='effect1_foregroundBlur_6113_7068'/%3e%3c/filter%3e%3cradialGradient%20id='paint0_radial_6113_7068'%20cx='0'%20cy='0'%20r='1'%20gradientUnits='userSpaceOnUse'%20gradientTransform='translate(-43.0144%20248.324)%20rotate(-25.0248)%20scale(462.733%20514.489)'%3e%3cstop%20stop-color='%23FF9DDA'/%3e%3cstop%20offset='0.44'%20stop-color='%23F7FF9D'%20stop-opacity='0.52'/%3e%3cstop%20offset='0.84'%20stop-color='%23FF8B7B'%20stop-opacity='0.2'/%3e%3cstop%20offset='1'%20stop-color='%23F7FF9D'%20stop-opacity='0'/%3e%3c/radialGradient%3e%3c/defs%3e%3c/svg%3e)

This decade will be seen as a golden age when finance teams transitioned from accounting for what happened in the past to prompting the rest of the business with financial strategies. From playing budgetary Battleship to presenting the opportunities they see for that business unit. That’s the speed at which markets now move and the only rational response to the pelting onslaught of change. But who can these new strategy-minded finance executives look to for inspiration? It turns out, there have been plenty of CFOs who came before and led in this active manner. Only now, their behavior isn’t the exception—it is the rule, and a necessity.

This guide shares four stories of finance leaders whose input made all the difference in their companies transforming completely. It’s part of an ongoing project to document bold finance-led transformations. If you have a story, we’d love to hear from you.

Lululemon

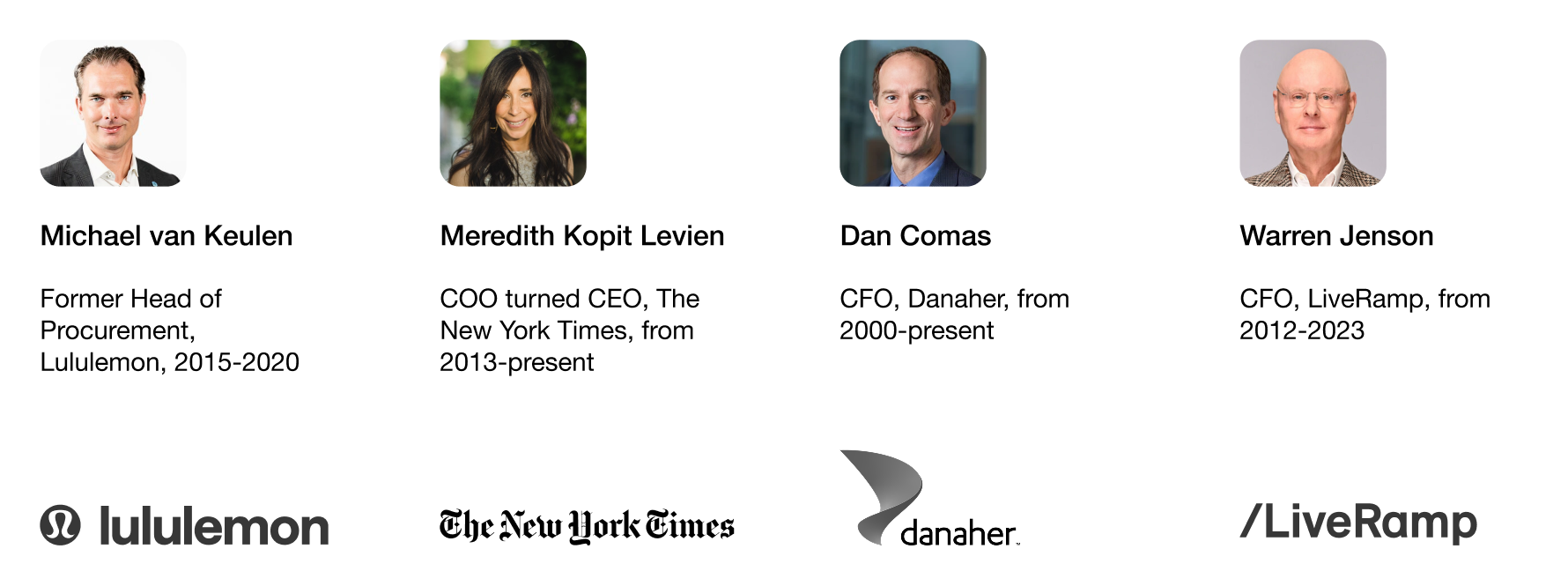

When Michael van Keulen joined as Lululemon’s head of procurement, procurement was not a strategic function. It was only purchasing. Just individuals pairing after-the-fact purchase orders to execute payments. The company did not solicit competitive bids, and often just used the same suppliers for 10 years without examining their ownership structure or locations. There was so much to change that Michael looked for a key item to challenge what he knew would strike an internal nerve—and chose shopping bags.

Lululemon regarded its distinctive shopping bags as a prized marketing asset. People grated at Michael’s questions about them. This filtered up to the CEO who voiced everyone’s concerns live, in an executive leadership meeting. Didn’t Michael understand how important the bags were?

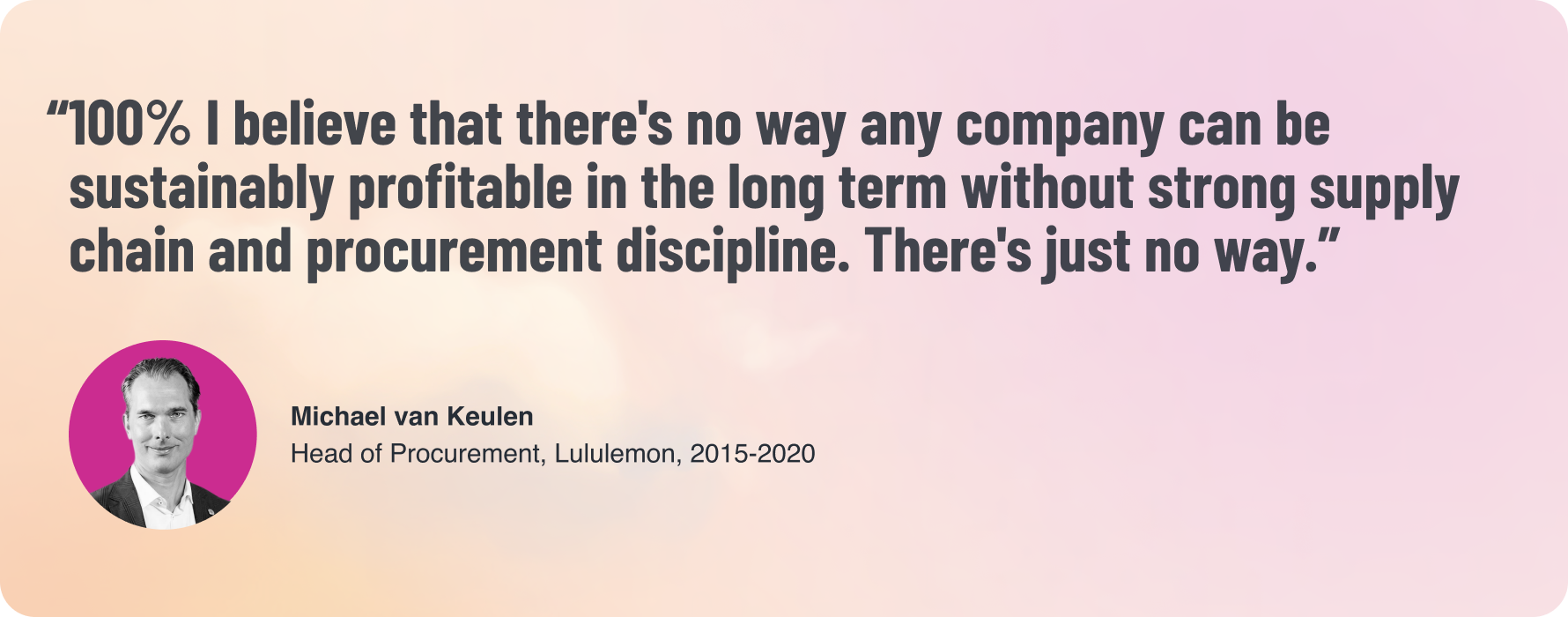

“I said ‘Well it’s interesting you say that. Do you know where they come from?’” says Michael. “And he looked at me. I said, ‘Well if it’s so strategically important I assume you know where they come from, how many we buy, how they are made, and how long it takes from factory to store.’ He didn’t know, and why would he? In reality, we were single sourced for all 20 million bags with one company in Cambodia where we were their sole customer with a nine-month lead time. ‘Do we think 08 | 4 tales of finance-led transformation that’s a good idea?’ I asked. ‘What if there’s social unrest? Cambodia is communist. What if the U.S. applies tariffs?* This is why you hired me, and oh by the way we have identified $4 million in savings, we’ll get the bags faster, they’ll be more sustainable, and we can reinvest that into the store experience.’”

That was the first salvo in educating the company on how procurement’s job is to deliver value, not just savings. “I can be blunt because I am Dutch, yeah?” says Michael. “People expect that. It’s how I am.” He began to hire, trained others, and deployed a spend management software that consolidated multiple buying platforms into one. This got stores out of doing their budgets in Excel, and provided something much closer to a source of truth for sourcing and procurement data. Each new system created a new information flow, which helped procurement identify new opportunities.

For example:

The company was unnecessarily buying their mannequin molds.

They weren’t selling third-party gift cards in big box stores—a sizable opportunity.

Most indirect contracts were non-competitive.

He could funnel no-loss procurement savings into an improved guest experience.

Michael deployed a strategy for winning each department over: Any savings he found, 50% would go to the bottom line and the balance would go into projects to accelerate growth. This allowed Michael to position his work, not as slashing people’s budgets, but offering them more working capital. The savings bought them better flooring, mannequins, shelving, placements, and training, which increased sales. They implemented new ecommerce features like buy online and pick up in store and, at Michael’s insistence, a gift card program in bigbox stores that still generates significant revenue today.

Michael’s procurement transformation playbook:

Challenge a sensitive category right away: This allows you to draw attention and use it as a moment to educate.

Don’t focus on savings, maximize value: “Savings diminish. After 2-3 years, you’re out of tricks. My goal is not to save money. My goal is to create value—to de-risk, reinforce, find better quality, negotiate better payment terms, and drive innovation. And yes, sometimes we save money.”

Lead from behind and don’t overstep: “My job is to provide options. To say, ‘If we change to a new supplier, here is the impact on working capital. Better quality, better lead time. But downsides too.’ Ultimately the business decides.”

The New York Times

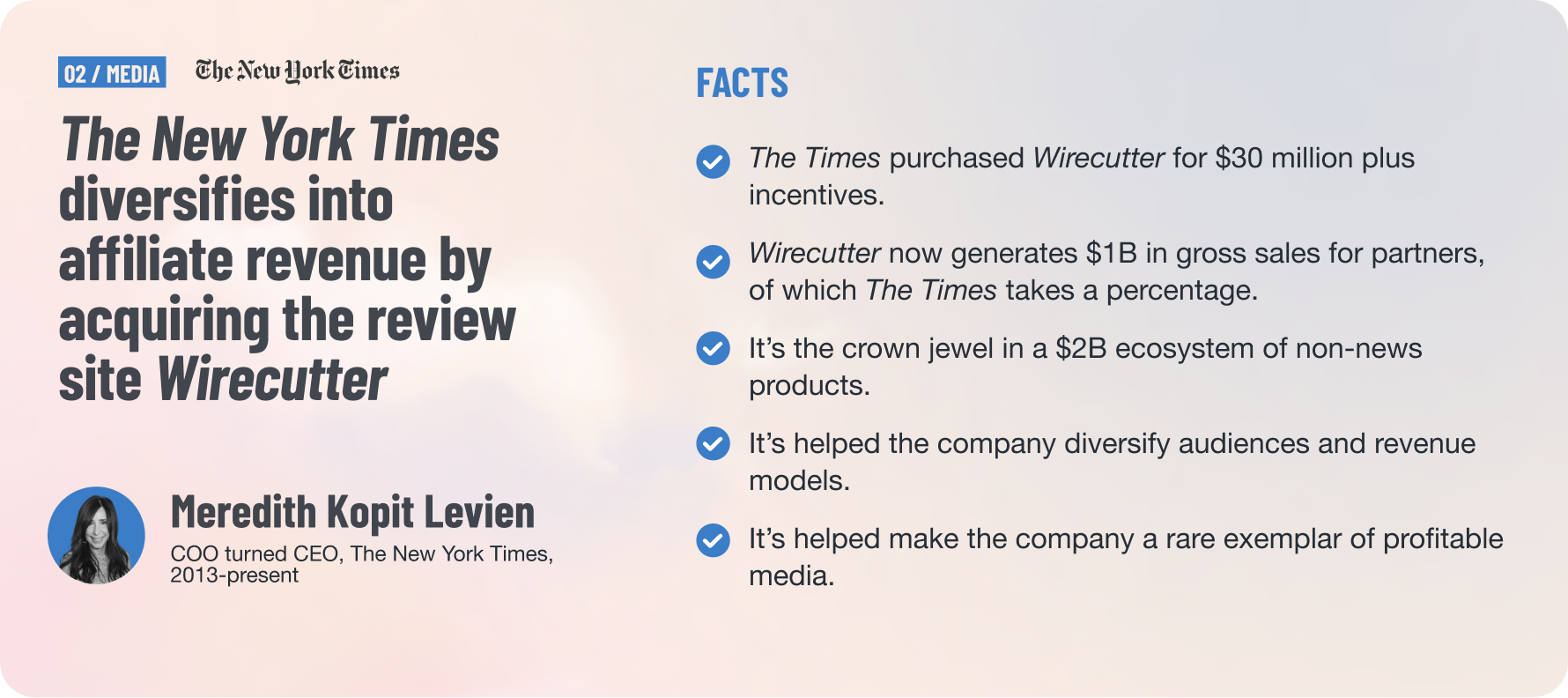

Newspapers were struggling long before 2016, when The New York Times chief operating officer Meredith Kopit Levien advocated for buying the consumer tech review site Wirecutter. The purchase quickly proved prescient and kicked off a decade-long expansion into affiliate and direct-to-consumer subscription acquisitions with two distinct qualities:

Continuous, self-reinforcing revenue growth

Mission alignment to The Times’ core journalism

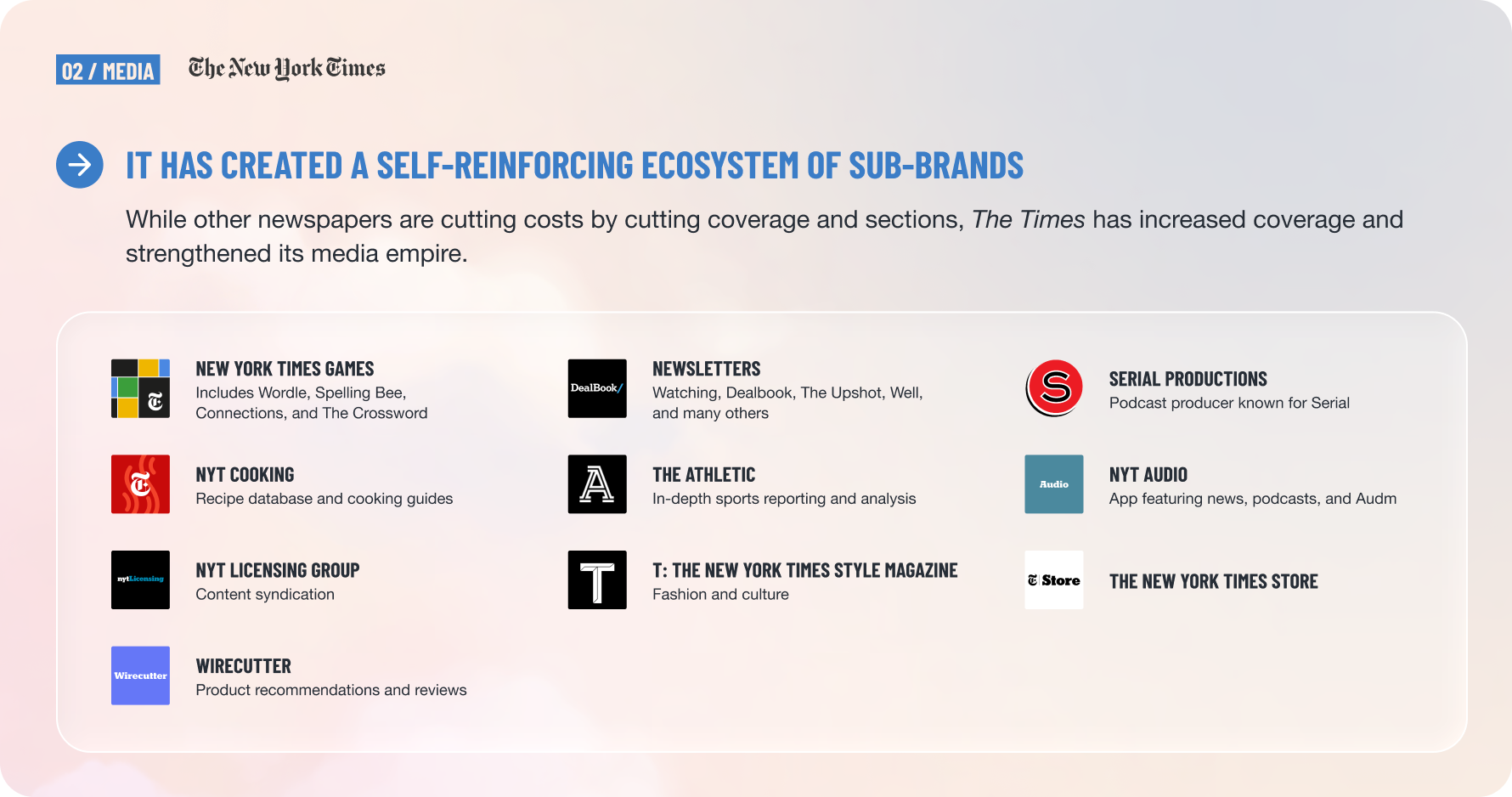

As The New York Times former VP of advertising, Meredith wanted the paper to become known for more than just journalism—every paper’s dream. That way, they could build loyal fanbases around new offerings with something for everybody. Wirecutter was the first in what would become a string of purchases or projects to build out that portfolio.

For the culinary-inclined, there was NYT Cooking. For commuters, The Times purchased the podcast studio Serial Productions. When a lone developer created a word-completion game called Wordle for his fiancée and it shot to the top of the App Store, the paper’s corporate development team quickly purchased it and folded it into their games section. No other U.S. newspaper has de-risked its reliance on advertising and news subscriptions so thoroughly. It is the chief reason The Times has been so financially successful compared to other media. In 2020, Meredith was promoted to chief executive officer.

Let’s unpack what made Meredith Kopit Levien’s purchase of Wirecutter so clever:

It helped the legacy paper diversify away from ad revenue: At the time of the purchase, The New York Times ad revenue had tanked. It was exposed to an ad model that relied on web traffic, which Google and Facebook were quickly gobbling up. The Times started by launching its flagship digital subscription. Its next step was to purchase Wirecutter to access affiliate revenue from megastores like Amazon and direct-to-consumer advertisers who didn’t traditionally advertise in papers.

The company’s advertising revenue has held constant for the past decade at $500 million per year, while overall revenue has nearly doubled. In 2016, advertising accounted for 37% of the company’s revenue. By 2025, it was down to less than 20%. In 2016, advertising accounted for 37% of the company’s revenue. By 2025, it was down to less than 20%.

Wirecutter was mission aligned and set the tone for further acquisitions: Wirecutter was known for rigorous reviews and journalistic transparency, just like The Times. Had the company purchased a less scrupulous aggregator, one imagines the strategy wouldn’t have worked. Readers and journalists would have balked at the paper’s erosion of morals. The recent trouble The Washington Post has experienced, a top competitor, bears this out when the new owner announced they’d be censoring the editorial section, the paper lost a reported 60,000 subscribers.

“Trust is part of the business model.” - Cliff Levy, Deputy Publisher, Wirecutter

The purchase helped The Times get savvy on alternative revenue models: The infusion of talent helped push the aging paper to experiment more. After the acquisition, Wirecutter launched a Google Shopping partnership where Google featured the site’s reviews on back-to-school gear. The New York Times has now launched half a dozen additional subscription options and newsletters such as The Athletic, which can feature Wirecutter articles. They’ve pulled Wirecutter articles into the core paper, and stretched the paper’s overall ad platform back over sites like Wirecutter.

Danaher

Danaher started out in the 1980s as a slow-moving real estate trust, but quickly changed hands. The new owners brought a fire of renewed purpose and an interest in complex products and manufacturing. By chance, they outbid a rival to acquire a manufacturer in healthcare—Chicago Pneumatic—which would set a tone for the hundreds of acquisitions to follow.

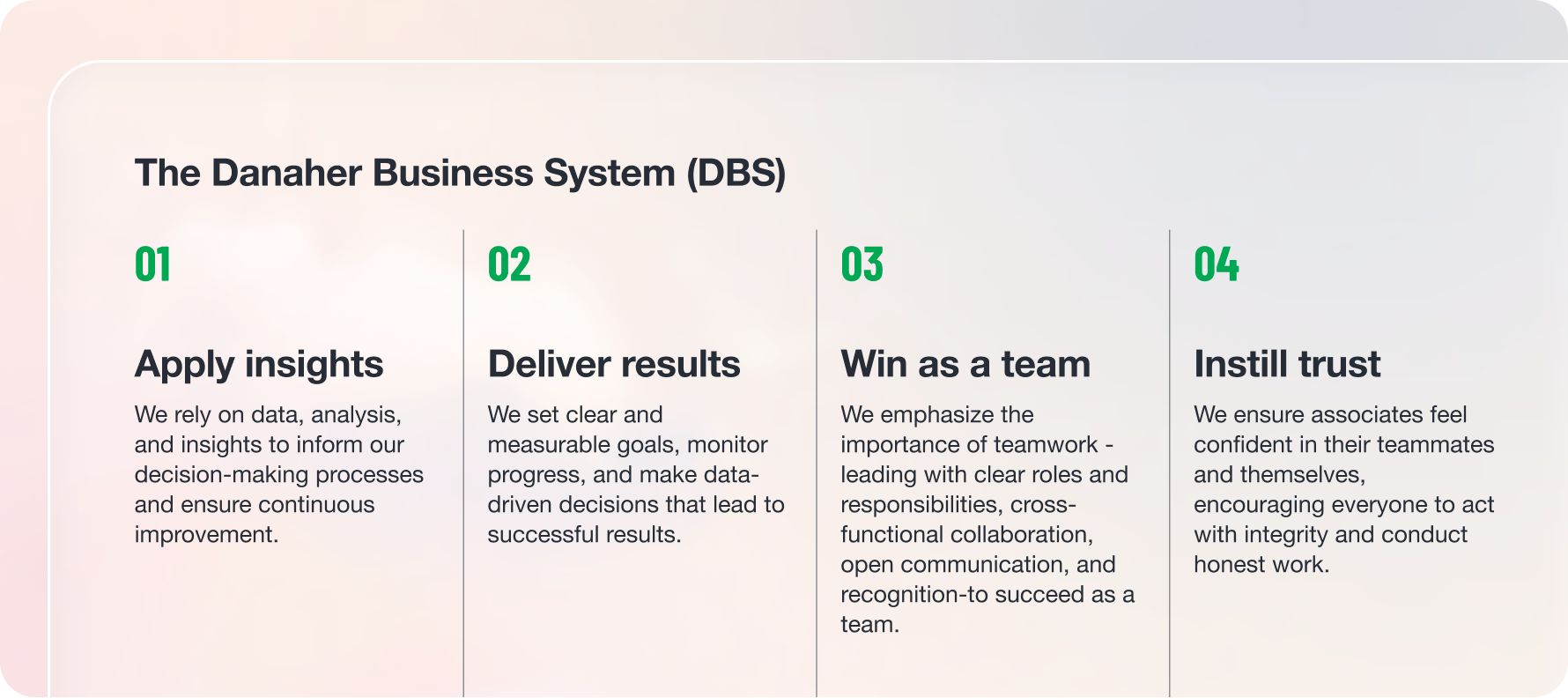

At first, their strategy was to find underperforming manufacturers that held useful intellectual property, buy and reorganize them. This worked because Danaher’s owners were experienced operators who’d developed their own proprietary methodology for running businesses, the Danaher Business System (DBD), based on Toyota’s production system and lean manufacturing.

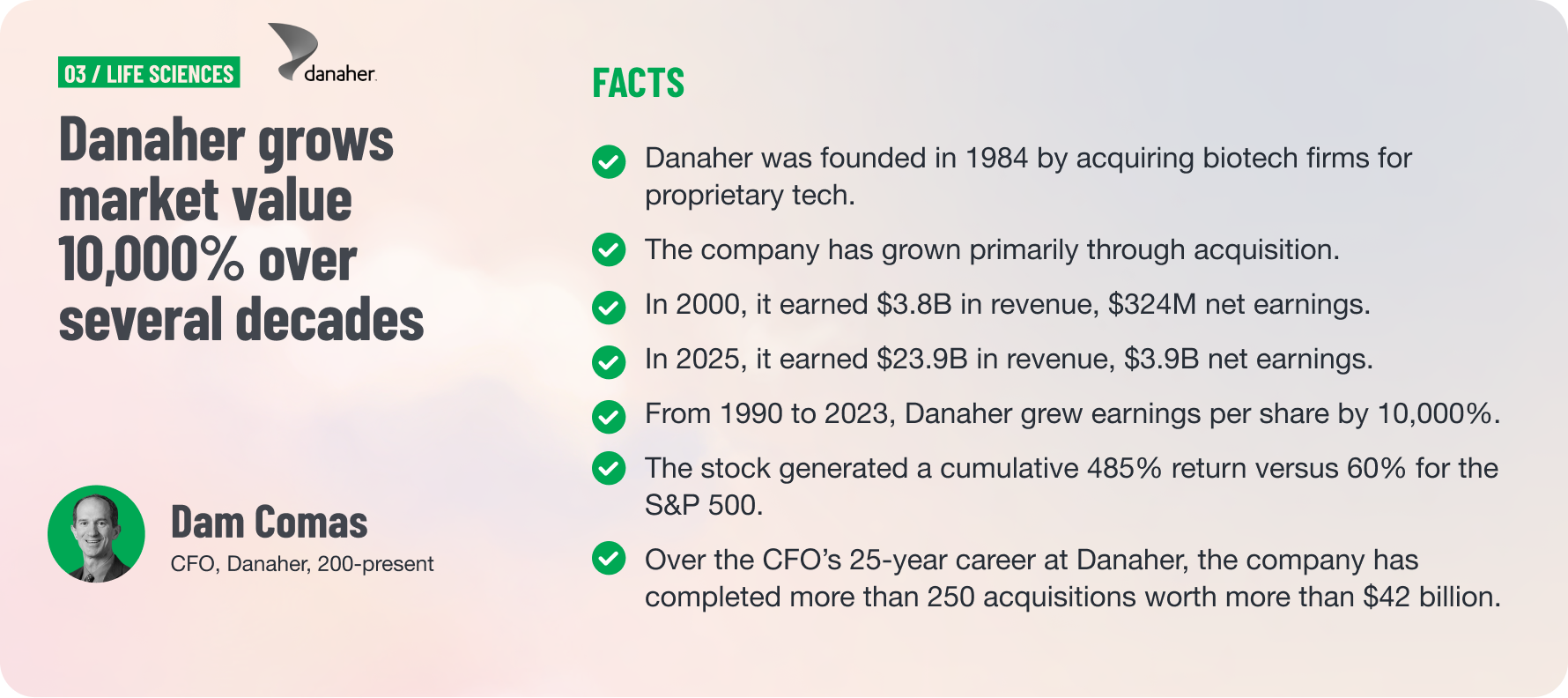

That strategy worked for a time. But they were implementing lean systems in businesses that were highly susceptible to market cycles. By 2000, the strategy had run its course. Dotcoms crashed and the U.S. economy contracted. Danaher recorded a nearly $70 million restructuring charge, and revenue fell 11%. The then CEO announced a plan for an “act two”: switching to acquiring businesses not subject to market cycles—in printing, water quality, and medical devices. Then VP of corporate development Dan Comas, in his fifth year with the business, took charge.

Dan started orchestrating dealflow. They made their first medical monitoring acquisition in 2004, with Radiometer, and when their integration strategy worked quicker than expected, Dan was appointed CFO, with a broad scope—he was EVP, led Finance, accounting, tax, corporate development, investor relations, IT, procurement, and treasury. He and the CEO shared a vision to make Danaher into a medical device company, and Comas showed an unusual skill for amassing capital and holding it so they could pursue that strategy during downturns. Buying in down markets spared them the typical debt load and let them integrate companies quicker. Along the way, they refined their purpose: Their biotech, medical, and life sciences hardware acquisitions did the best, especially after they applied DBS, so that became their overall focus. That focus cleared the way for more acquisitions. In 2009 alone, they purchased 18 companies.

In two decades, Danaher has evolved from a cyclical industrials company into a scientific and technical instrumentation company competing in less cyclical markets. The company has completed 250 acquisitions during Comas’ 25-year tenure, and in that time, the stock price has risen 10,000%. In 2025, their net earnings exceeded their total revenue from the year 2000, when Comas started his work.

Danaher's M&A growth strategy worked because:

They had a deep operational advantage: The DBS system let them find efficiencies beyond the typical layoff playbook, which left the companies stronger. It doesn’t promise magic—just an additional 10% market value and more patents. But applied across all the portfolio companies, it makes talent and knowledge interoperable and transferable between its 24 locations and 60,000 employees.

Hoarding capital and the discipline to wait to buy in a downturn: Danaher’s finance team has shown uncommon discipline and fortuitous market timing.

They found the synergies along the way: Hundreds of acquisitions have sifted down into just 15 portfolio companies. That took a lot of integration work and rigor, but the narrowed focus into biotech and medical devices gave them an increasingly strong thesis and foresight.

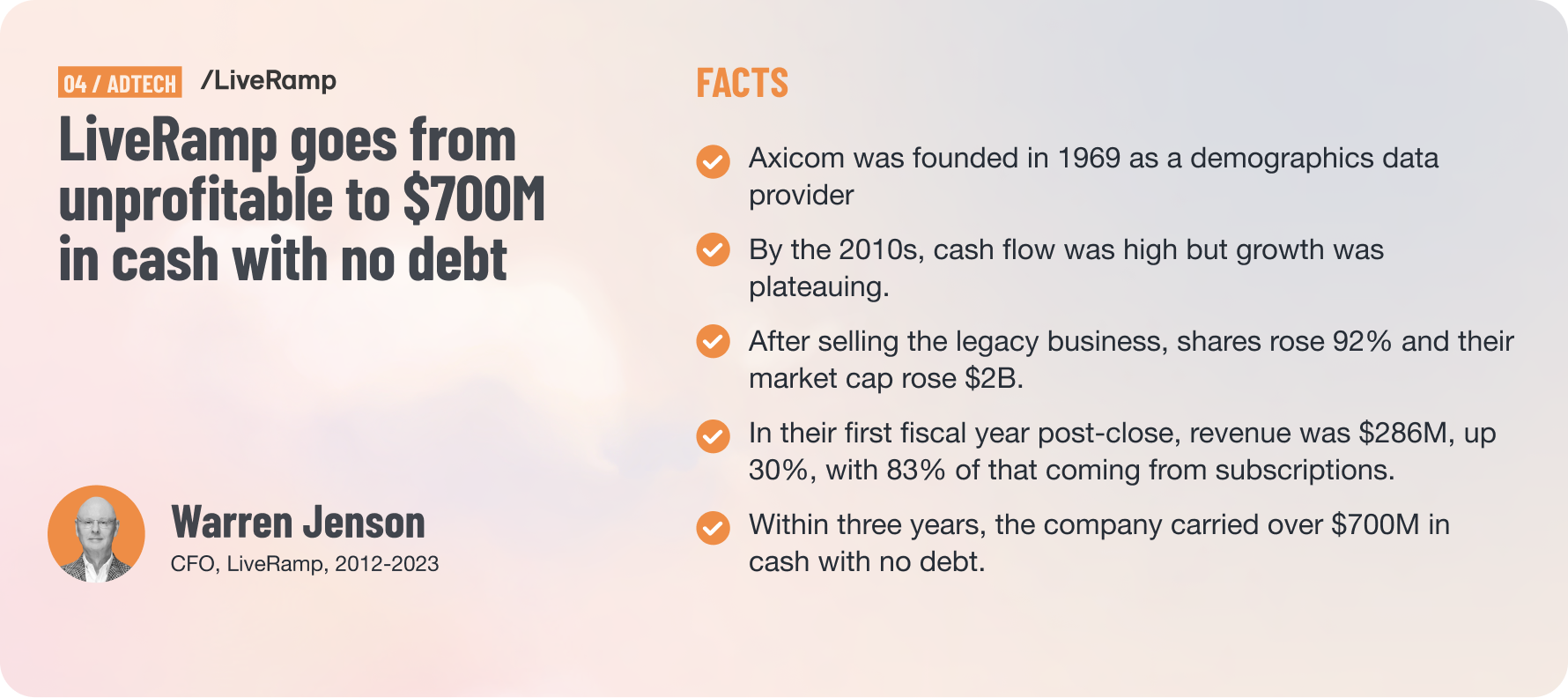

LiveRamp / Acxiom

In 2014, the database marketing firm Acxiom purchased a fast-growth tech startup, LiveRamp. Their new-ish CFO Warren Jenson had previously been CFO at NBC, Delta Airlines, Amazon, and Electronic Arts, and he brought with him a vision so large, it couldn’t have come from within the company. He wanted to apply all he’d learned in his prior roles with M&A and divestitures to see if he could help the company generate far more value for shareholders than a public relations firm had any right to do. Hence, he helped lead the acquisition of the tech company LiveRamp.

LiveRamp was an advertising identity platform with a lot of future potential but which was “still in startup mode,” says Warren, and losing cash. For several years, the executive team explored how best to integrate it into Acxiom and realized that investors were still seeing two different companies patched together. “Acxiom Marketing Solutions was our slowgrowth, high-touch service business that generated a lot of cash,” says Warren. “LiveRamp was our high-growth SaaS platform … and through our analysis, we learned that divestiture could unlock more value for both companies.” But the planned divestiture wasn’t LiveRamp—it was Acxiom.

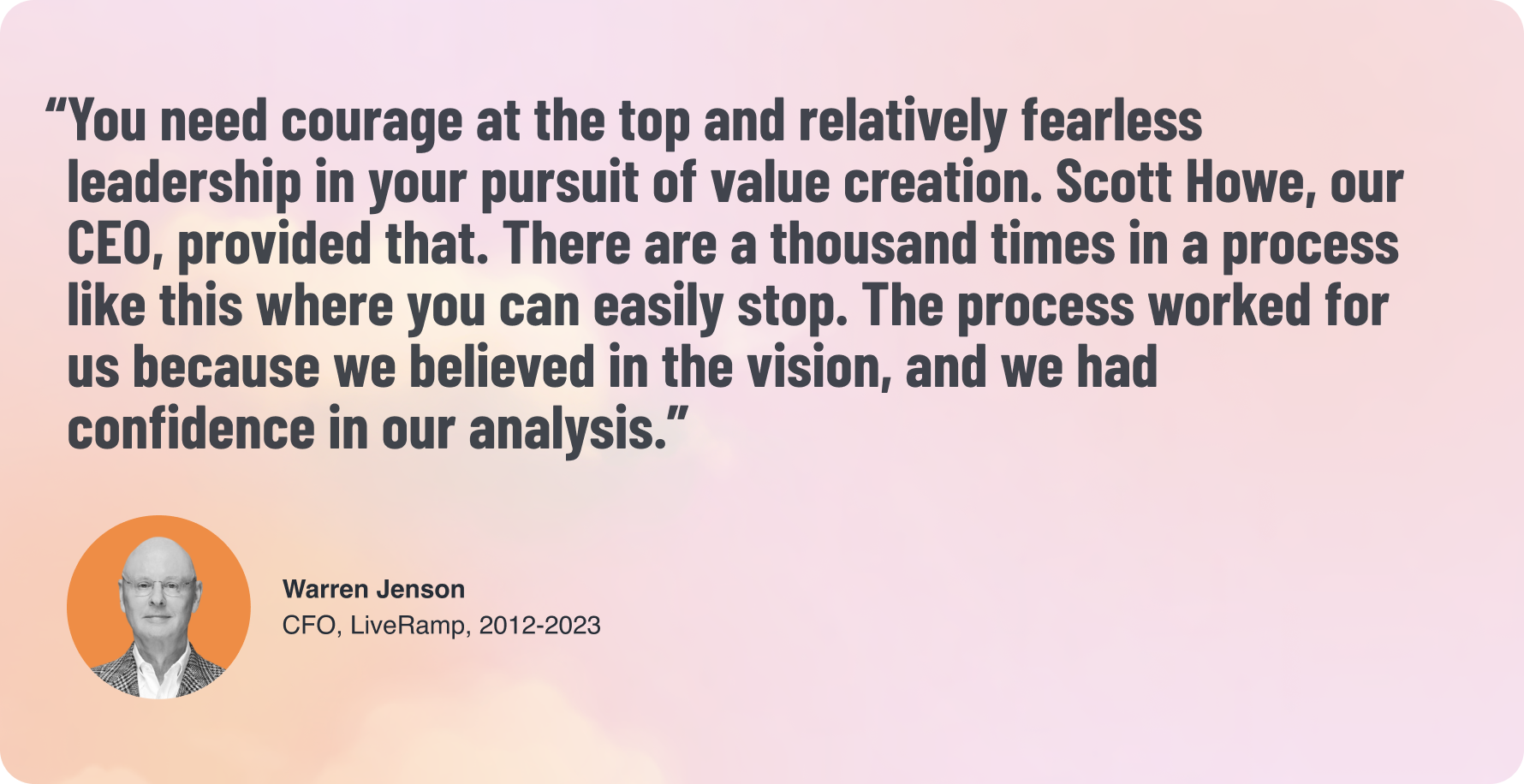

It is worth pausing to reflect on the audacity of this decision. To slough off 100% of cash flow and 75% of employees to bet on a money-losing startup in investment mode took immense resolve. But Warren and his team were confident in the numbers. “You need courage at the top and relatively fearless leadership in your pursuit of value creation. Scott Howe, our CEO, provided that. There are a thousand times in a process like this where you can easily stop,” says Warren. “The process worked for us because we believed in the vision, and we had confidence in our analysis.”

They began to plan the carve-out long in advance—which Warren says was key. For two years, they backpedaled on the integration and strove to make each entity self-sufficient. “When you’re defining a carve-out, remember that everyone has to win; both companies need to come out of the process strong and healthy,” says Warren. His accounting team generated complete auditable financial statements for each entity. They analyzed all the carve-outs carefully and ran endless, complex financial modeling for every financial and operational scenario.

When the time came in 2017 to announce the divestiture, they already had a data-backed valuation range and ready answers to every investor question. They announced the strategic move in February, found a buyer in July, and closed the deal in October.

As part of the transition, the newly singular LiveRamp documented more than 125 transitional service agreements and eight intercompany agreements. It used the $3.6B in sale proceeds to pay down its $230M in extant debt and switch over into growth mode on all fronts. Since 2018, the share price has more than doubled and they’ve returned $750M to shareholders. “And the best part is, Acxiom is flourishing under new shareholders,” says Warren.

Here’s what made the LiveRamp-Acxiom switchout work:

They listened to the market and investors: When it was clear that investors weren’t understanding the integration, Warren and the executive team didn't panic. They took that information in and thought about how to use it to their advantage.

They considered all options: In their rigorous modeling and scenario planning, they considered all scenarios, including one where LiveRamp never evolved into more than a medium-growth business. “When we announced that we were looking at strategic alternatives, we were open to anything that took us to our desired end state,” says Warren. “It could have been a partnership or a tax-free merger. It ended up being a sale, but we never closed any doors. Through our preparation, we not only protected but also increased our optionality and value.”

It all hinged on a foresight into the adtech market: As former CFO at NBC, Amazon, and elsewhere, Warren brought unparalleled insight into where ad-supported media was headed. He and the executive team bet everything on a technology that promised to do a better job at securely connecting, controlling, and activating advertising data, on the assumption that data regulations and pressure to show return on ad spend would lead companies to want that technology. That proved correct.

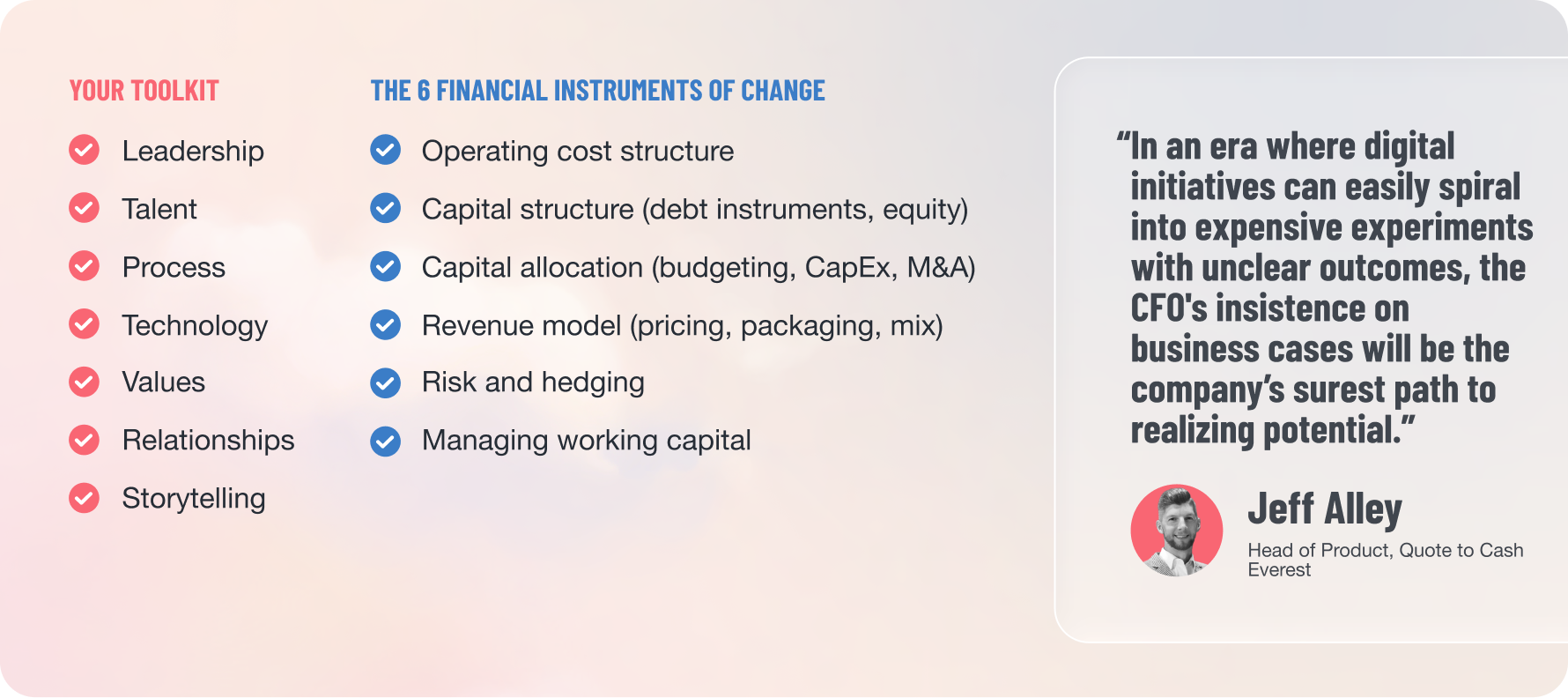

Are you ready to embrace you expanded remit?

There have always been finance leaders who led their company through major transformations—but it is becoming increasingly common. At the speed and rate of change, CEOs alone cannot surface every idea. And finance executives bring an expanded toolkit to bear to suggest new operating cost structures and M&A opportunities that might not have occurred to the chief executive. As this transition unfolds, it’s raising the value of strong, flexible financial software. To explore all options, to model complex scenarios, and to understand how market forces will affect your business, you need core systems that were built for change. That’s how you go from playing budgetary Battleship to presenting the opportunities you see for each business unit—and leading that change.