'%3e%3cellipse%20cx='185.202'%20cy='292.401'%20rx='236.2'%20ry='212.4'%20transform='rotate(180%20185.202%20292.401)'%20fill='url(%23paint0_radial_6113_7068)'/%3e%3c/g%3e%3cdefs%3e%3cfilter%20id='filter0_f_6113_7068'%20x='-130.996'%20y='0.000976562'%20width='632.398'%20height='584.8'%20filterUnits='userSpaceOnUse'%20color-interpolation-filters='sRGB'%3e%3cfeFlood%20flood-opacity='0'%20result='BackgroundImageFix'/%3e%3cfeBlend%20mode='normal'%20in='SourceGraphic'%20in2='BackgroundImageFix'%20result='shape'/%3e%3cfeGaussianBlur%20stdDeviation='40'%20result='effect1_foregroundBlur_6113_7068'/%3e%3c/filter%3e%3cradialGradient%20id='paint0_radial_6113_7068'%20cx='0'%20cy='0'%20r='1'%20gradientUnits='userSpaceOnUse'%20gradientTransform='translate(-43.0144%20248.324)%20rotate(-25.0248)%20scale(462.733%20514.489)'%3e%3cstop%20stop-color='%23FF9DDA'/%3e%3cstop%20offset='0.44'%20stop-color='%23F7FF9D'%20stop-opacity='0.52'/%3e%3cstop%20offset='0.84'%20stop-color='%23FF8B7B'%20stop-opacity='0.2'/%3e%3cstop%20offset='1'%20stop-color='%23F7FF9D'%20stop-opacity='0'/%3e%3c/radialGradient%3e%3c/defs%3e%3c/svg%3e)

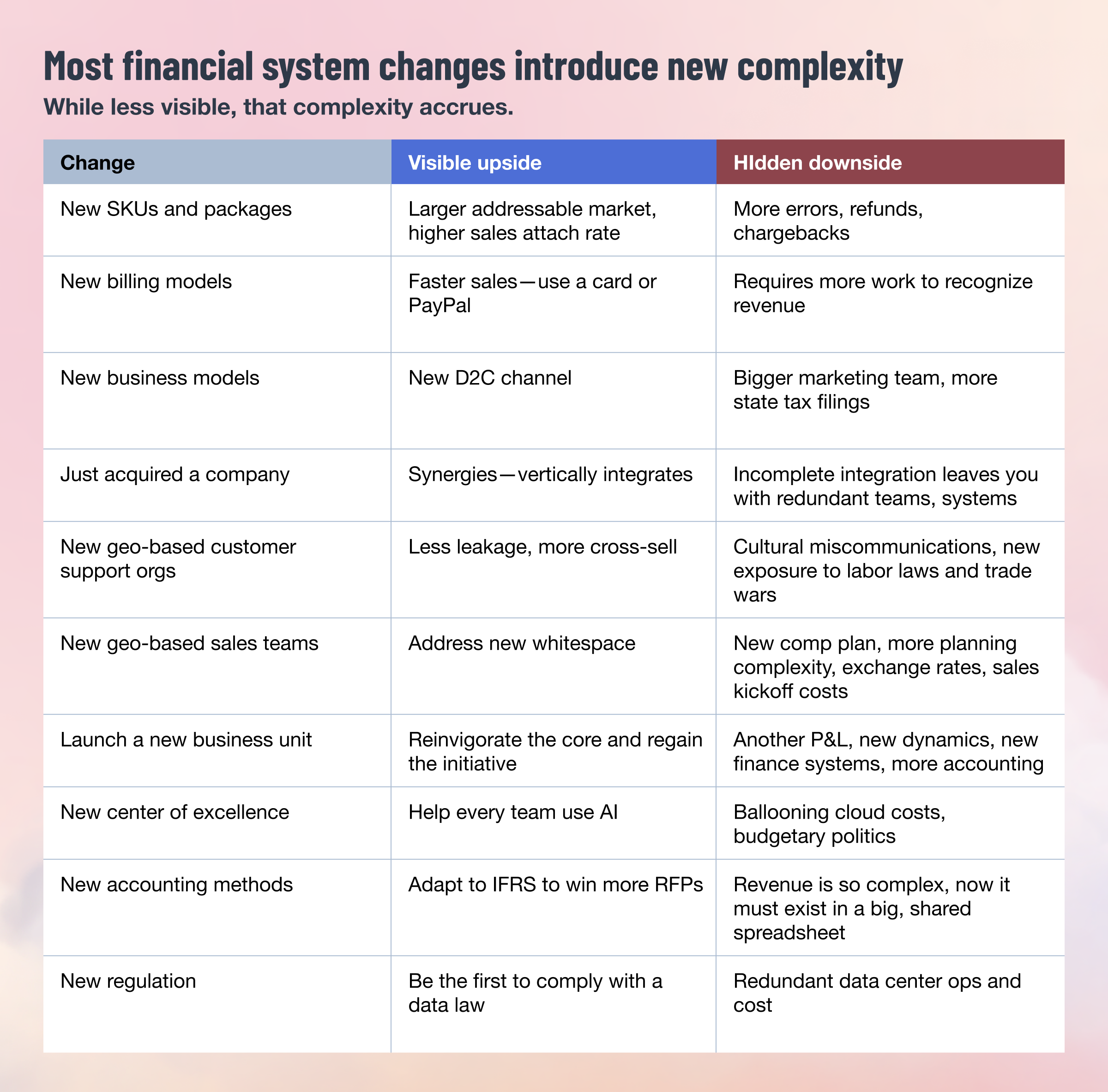

When it comes to financial systems, the ‘debt’ analogy works quite well. You take on complexity debt by over-configuring your systems because it helps you move fast. For example, say you hire a new sales leader who insists on closing a deal in Turkey, where you hadn’t previously operated. Your team scrambles to figure out foreign exchange rates and research taxes and tariffs and, in the rush, they add a bunch of required fields to your ERP as well as paragraphs to your agreements.

Every day thereafter, anyone touching the order-to-cash process operates 1% slower. You’ve taken on new system complexity and not rationalized it, and that compounds. Like debt.

Debt can be good, so long as it remains manageable. In this article, we explore this idea along with advice for keeping your ERP system functional. For more ideas, visit our latest guide: 30 lessons from 30 years of ERP.

Complexity debt is the sum result of all the changes you’ve made to your financial systems, and the impact on teams who use those systems

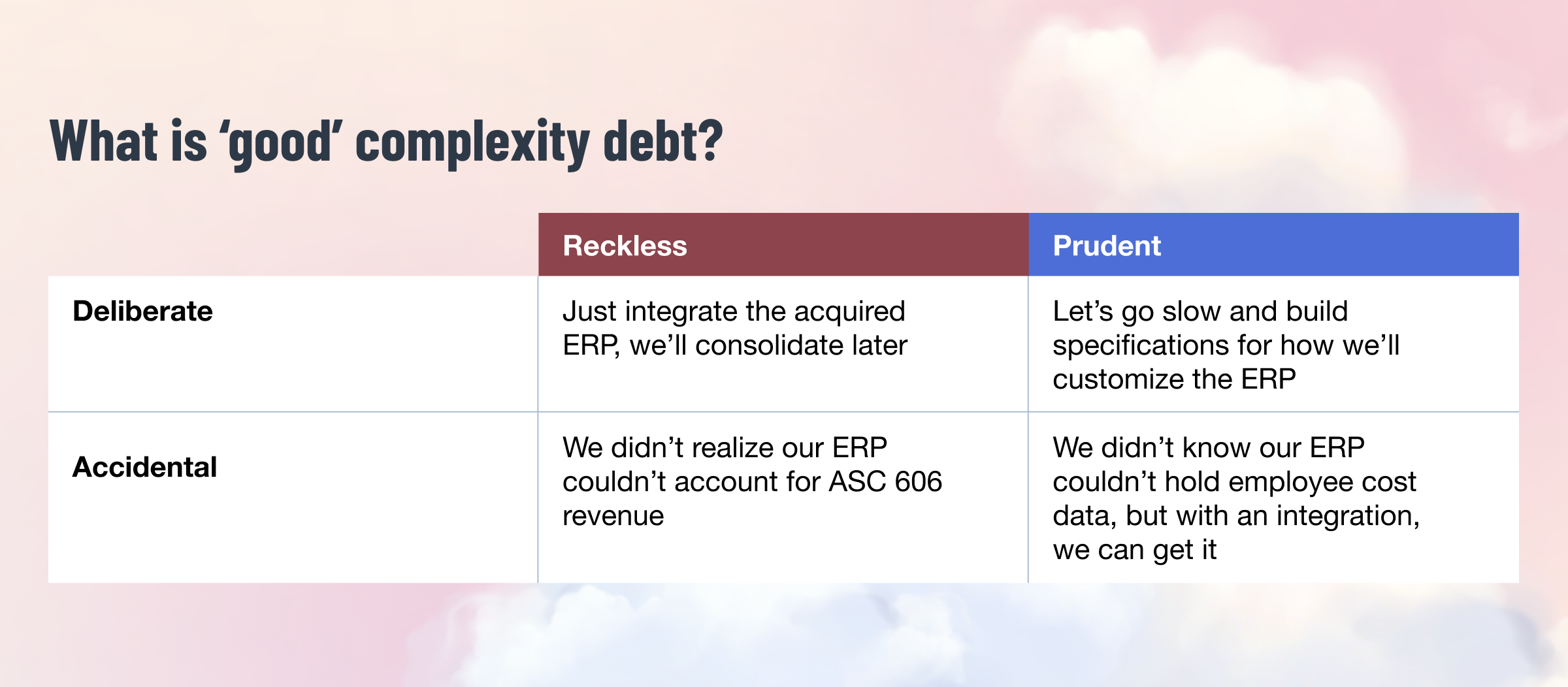

Rule 1: Complexity debt isn’t always bad—it’s a resource

You take on system complexity because it helps you move forward to launch a product, enter a new market, raise capital, or integrate a newly acquired company. It is your team adjusting your systems to better fit your market and customer. It is the evolutionary response to opportunity.

But while it is easy to quantify the value of making the change—“let’s add another SKU”—the costs are invisible. They are tiny inconveniences spread throughout your department and company. But they accrue. This partly explains why so many ERPs look smooth in a demonstration, but the actual implemented version is a war zone of neglect and misuse. The debt has matured and ruined that financial system.

You take on these types of complex debt because there’s a positive payoff. Just like financing.

Rule 2: Your complexity debt accrues interest

Complexity becomes a problem when it ceases to be serviceable—when it interrupts work. Though over time, workers normalize this toil. They accept having to answer a simple question about receivables, they have to look at three separate screens. It’s “just how work is done here.” But eventually the debt compounds and payments come due.

This is why you should periodically audit your debt. Enlist a senior finance manager and a business operations person who, together, audit all recent financial system customizations to help you understand what sort of debt you have. For example:

Can you even see the debt?

Tracking it isn’t easy but the effects are unmistakable: High debt systems frustrate employees who vent to others and build workarounds. You can see it in hostility to other teams and in overmany requests to buy new bolt-on software.

What is the sum of the debt?

Each complex-ifying choice seems small. But you have to look at how often interest is due. Add one step to the month-end close process, and soon, it takes six weeks. New steps beget more steps which makes it harder to train, hire, and retain people.

What’s the interest rate?

Estimate the time cost of the debt. How much does the spreadsheet workaround require to maintain, and how quickly will it grow obsolete? Does maintaining it become one person's whole job? Will it require offshore contractors or analysts?

What are the repayment terms?

How soon must you repay it? Do you have a grace period from now until the next fiscal year, or are the changes already taking a toll?

What’s your relationship to the lender?

What team effectively “pays” the debt? You can build your business systems to accept the cost yourself, say by making your accountants responsible for building reports for functional leaders. Or you can foist the debt on other teams by training them on the business intelligence tool and asking them to self-serve. Debt is best spread evenly.

What can you restructure?

Making iterative changes to your business systems sounds reasonable. But sometimes you apply fixes to fixes and build yourself into a corner. The more everyone has to explain the workflow and keep a big PDF of screenshots, the more acute the cost.

Good business operations teams know to stop debt at the source. They reinterpret new requests while considering the whole of the debt—instead of doing as instructed, they ask, “What are you trying to accomplish?” They may place a freeze on new ERP and CRM changes to assess debt and pay it off, saying, “If you give me a quarter, I’ll save your team that much time every quarter.”

Good debt is the kind that gets you ahead and is serviceable. The rest, you should address.

Rule 3: Pay down high-interest debts first

The high-interest, unsustainable debts are never secrets—not if you talk to your team. They show up in water-cooler talk and at performance review time. Other teams will express frustration that your team is blocking them. Say the revenue organization wants to launch new sales territories or change vendors, and your analysts can’t pull the numbers in time. Or maybe the customer service org is over-hiring because they can’t edit contracts once they’re in the system, and any minor scope change is a big, drawn-out process.

When paying down debt, start with the most visible pains. And consider that in some areas of the system, bankruptcy is an option. It’s not necessarily the end—it’s you putting a name to the problem and entering a restructuring period where you get to redesign the process maps and software. Sometimes, that means reevaluating your ERP because through your audit you have realized, as Primary Health did, that 80% of your critical workflows run through spreadsheets. In which case, isn’t the ERP just functioning like an expensive database? And wouldn’t a data lake be cheaper?

The best way to manage complexity debt is to become aware of it

Perhaps you know complexity has a cost, but don’t know the specific sum. Here is a simple test: If you find that adding more people and tools tends to slow work down even more, there’s likely a complexity issue. That issue could lie with people, processes, or tools. The best way to find out is to run a time study and figure out where precisely people are spending their time, and then decide whether you think it’s a good use.

Not all manual workflows are bad, either. Perhaps they present an opportunity for a real expert in tax law to find you new opportunities, like converting a warehouse into a foreign trade zone. And not all complexity debt is bad if it helps you close a big deal with a new spotlight customer. But do draw your attention to that total debt sum, and manage it accordingly.